The need to own a car by the US residents is practically essential in order to have an efficient and convenient travel from one place to another. Whereas the residents are working hard to ensure that they buy their dream cars, it has sometimes become daunting to successfully be able to buy the cars at the right time from personal savings. Hard economic times and poor budgetary controls have exacerbated the situation.

These factors have resulted to appalling personal saving behavior. In fact, many people are struggling to be in charge of their finances. However, financial institutions have provided a respite to the residents. Today, these financial institutions are more than willing to offer car loan financing and have put in place desirable measures to ensure that every citizen owns a car of choice. Car loans can be categorized as secured or unsecured.

Secured car loans car be defined as those that required collateral to be placed by the borrower. Collateral is an asset or item that is used as a security for the loan in case of an uncertainty repayment. Secured loans are offered based on the historical financial records of the borrower and other external factors, which may be beyond the control of the client.

These external factors include economic stability, political environment, and market trends. Where a client has unappealing previous financial record, this makes the car loan companies to take precautions against bad debts they may incur from failure to repay the loan. Consequently, due to their characteristics, secured loans are preferred because they usually attract low interest rates and are paid for in a relatively longer periods.

Mainly, the timeframe to repay secured loans may range from one year to six or more. When a client puts in place other considerations such as personal financial stability and income, they opt to borrow secured loans to be able to repay with ease. With a sound personal cash management, the clients can comfortably be able to pay the loan amount.

However, this kind of a loan has a disadvantage in that, incase the client fails to repay the loan, the collateral placed as security is confiscated by the car loan company. With secured auto loans, the possibility to loose the asset or item placed as security by the borrower is as high as the failure to repay the loan may occur.

It thus requires one to be self-disciplined in financial matters. It also assumes that other external factors beyond the person's control will not come by the way and cause financial breakdown. For instance, the retrogressive economic growths experienced all over the world between 2007 and 2010 displayed an ideal example where borrowers were driven to financial dark pits due to the prevailing unfavorable economic situations.

Many people lost their jobs, businesses shut down, and personal debts increased. The ability to repay secured loans was hampered. Collaterals were repossessed by the financial institutions. This left many auto loan clients bamboozled by the wary events.

Secured loans also limit the ability to borrow another loan in the near future, as one may need. This is because it takes a long time to repay the loan. Clients ‘shy off’ from multiple borrowing due to the repercussions attached to it.

Moreover, it becomes difficulty should a need arise that requires borrowing. When making that vital decision on which loan to undertake, one should put into considerations factors such as how soon one might need to borrow again, how stable the economy at large is, and how disciplined one is in personal financial management. Secured loans can help you acquire credit facilities at a lower interest rates compared to unsecured loans.

Friday, January 17, 2014

What are the Benefits of Online Banking

As technology advances so are the financial institutions operations. Today people can do their banking right from the office or in their homes. Applause to the technology developers who have made it possible to carry out online banking! It is today convenient to log on to the internet and initiate a transaction from the comfort of your home in any hour of the day. Isn't it amazing? Online banking has herald a technological cutting edge in the 21st Century.

The digital edge is not a myth as the legwarmers would perceive during those old days, but it has become a reality. There are no bank queues. Often clients are not kept in the contention of the laws that Graham forgot to mention, that the "other queue moves fast when you jump into another"

The days are gone when clients used to make long queues in banks lining for services with impatience. This has been molded into a click of a mouse and the bank service is self initiated. There are certainly no bank holidays as a client can transact a business, make or receive payments on the peak hour of the weekend.

Online banking offers more security than the conventional banking in the sense that no paper works that may scatter around and expose ones bank details. Similarly, other people cannot overhear conversations and get their details. With advancement in technology, it is easy to view statements.

With a click of a mouse, the customer can access details of the bank accounts, which include the account balances, the transactions initiated, as well as the dates of transactions. The customers can easily move cash between accounts. Making payments to clients such as suppliers is well tailored and fast to carry out. Cheque books and statements can be ordered easily.

The cost of effecting a transaction is one feature that customers look out for. The charges that are imposed for transactions in online banking are lower than those of the traditional banking. Convectional banking is often rendered expensive due to the logistics of operation.

It also requires that one travel to the bank to make their transactions. It's inefficient, time consuming and cumbersome. With the development of mobile banking, it is even more convenient. The incorporation of banking, internet and mobile phones has further customized online banking to the interests of the clients.

Although the online banking is faced with the challenge of insecurity due to the crop up of a new trade in fraudulent activities, the benefits are more than the challenges of insecurity and clients opt to take precautions. No in any time of history, has banking been made easy, friendly, convenient, and well tailored to the customer than in the online banking.

As people become occupied in other activities, time becomes a scarce resource and in order to beat this challenge, digital age has provided a solution for this through online banking. In essence, there are many benefits of online banking ranging from safety, convenience, and cost to flexibility.

The digital edge is not a myth as the legwarmers would perceive during those old days, but it has become a reality. There are no bank queues. Often clients are not kept in the contention of the laws that Graham forgot to mention, that the "other queue moves fast when you jump into another"

The days are gone when clients used to make long queues in banks lining for services with impatience. This has been molded into a click of a mouse and the bank service is self initiated. There are certainly no bank holidays as a client can transact a business, make or receive payments on the peak hour of the weekend.

Online banking offers more security than the conventional banking in the sense that no paper works that may scatter around and expose ones bank details. Similarly, other people cannot overhear conversations and get their details. With advancement in technology, it is easy to view statements.

With a click of a mouse, the customer can access details of the bank accounts, which include the account balances, the transactions initiated, as well as the dates of transactions. The customers can easily move cash between accounts. Making payments to clients such as suppliers is well tailored and fast to carry out. Cheque books and statements can be ordered easily.

The cost of effecting a transaction is one feature that customers look out for. The charges that are imposed for transactions in online banking are lower than those of the traditional banking. Convectional banking is often rendered expensive due to the logistics of operation.

It also requires that one travel to the bank to make their transactions. It's inefficient, time consuming and cumbersome. With the development of mobile banking, it is even more convenient. The incorporation of banking, internet and mobile phones has further customized online banking to the interests of the clients.

Although the online banking is faced with the challenge of insecurity due to the crop up of a new trade in fraudulent activities, the benefits are more than the challenges of insecurity and clients opt to take precautions. No in any time of history, has banking been made easy, friendly, convenient, and well tailored to the customer than in the online banking.

As people become occupied in other activities, time becomes a scarce resource and in order to beat this challenge, digital age has provided a solution for this through online banking. In essence, there are many benefits of online banking ranging from safety, convenience, and cost to flexibility.

Tuesday, January 07, 2014

Do Car Insurance Companies Take Advantage of Good Drivers?

The subject of car insurance companies and the payment of premiums continue to draw out debates on how companies benefit at the expense of their clients. Have you asked yourself this question; what happens when you buy car insurance coverage and you don't cause an accident in the entire lifetime? The answer to this question is as perturbing as to the lack of knowledge as to when you will cause or be involved in an accident.

A client remains in suspense of knowing when an accident will strike next. Although it is not within the desire of motorists to be involved in accidents, it is sometimes a bother to the insured when they pay insurance coverage only to remain uncompensated for injuries or damage to a vehicle due to good driving ethics.

Whether it's a good luck or simply an act of observing good driving ethics, the implication is that car insurance companies benefit at the expense of the insured when they do not cause accidents. Often the insurance companies have used the driving history as one of the main determinants of the insurance premium rates determinants.

Bad driving ethics characterized by subsequent accidents usually hike the premium rates and the insured bears the burden of bad driving practices. But then, what happens when an insured does not cause or is not involved in any way in accidents that warrant compensations?

As an appreciation of good driving ethics, insurance companies impose reduced rate of premiums to the insurance buyers. However, the company keeps attached to the assumption that the driver will at one time be involved in an accident thus has to keep on remitting their premiums. Nonetheless, the drivers keep on observing good driving behaviors and do not cause accidents that warrant compensations to be made. In this case the car insurance company benefits from these remittances and in fact there are no refunds that are made.

Insurance companies operate on a notion that, even if an insurance buyer is not compensated for any injuries or car damages, others are paid for the same. The success of the insurance company is based on the fact that only few drivers will cause accidents and claim for compensations. This is where the whole issue of car insurance payment becomes complex and often regarded as unfavorable for the drivers who observe an accident-free driving.

In fact some drivers have attempted to cause accidents so as to place a claim for compensation because they perceive that their good ethical driving practices as a benefit to the insurance company. Whether this is a justifiable act or not, the issue is that insurance companies should consider revising the way good drivers are rewarded for their good performance.

It is worthwhile mentioning that, car insurance companies and governments should get back to the drawing board and bring out a concise and clear answer to this heated debate. To grab the bull by its horns, insurance buyers feel betrayed by the insurance companies especially when they do not indulge in accidents that prompt the companies to reimburse compensations. The government must analyze this aspect and bring out a more customer oriented car insurance policy.

Auto insurance buyers who in most of their life time do not assume compensations of any nature during their driving history are dissatisfied by the way insurance companies use their premium contributions for their sole benefits. Aptly, there is a burning issue that needs to be resolved and this is; should insurance buyers receive a considerable amount of refund if they do not cause accidents or are not in any way compensated for personal body injuries or car damages within their driving experience?

A client remains in suspense of knowing when an accident will strike next. Although it is not within the desire of motorists to be involved in accidents, it is sometimes a bother to the insured when they pay insurance coverage only to remain uncompensated for injuries or damage to a vehicle due to good driving ethics.

Whether it's a good luck or simply an act of observing good driving ethics, the implication is that car insurance companies benefit at the expense of the insured when they do not cause accidents. Often the insurance companies have used the driving history as one of the main determinants of the insurance premium rates determinants.

Bad driving ethics characterized by subsequent accidents usually hike the premium rates and the insured bears the burden of bad driving practices. But then, what happens when an insured does not cause or is not involved in any way in accidents that warrant compensations?

As an appreciation of good driving ethics, insurance companies impose reduced rate of premiums to the insurance buyers. However, the company keeps attached to the assumption that the driver will at one time be involved in an accident thus has to keep on remitting their premiums. Nonetheless, the drivers keep on observing good driving behaviors and do not cause accidents that warrant compensations to be made. In this case the car insurance company benefits from these remittances and in fact there are no refunds that are made.

Insurance companies operate on a notion that, even if an insurance buyer is not compensated for any injuries or car damages, others are paid for the same. The success of the insurance company is based on the fact that only few drivers will cause accidents and claim for compensations. This is where the whole issue of car insurance payment becomes complex and often regarded as unfavorable for the drivers who observe an accident-free driving.

In fact some drivers have attempted to cause accidents so as to place a claim for compensation because they perceive that their good ethical driving practices as a benefit to the insurance company. Whether this is a justifiable act or not, the issue is that insurance companies should consider revising the way good drivers are rewarded for their good performance.

It is worthwhile mentioning that, car insurance companies and governments should get back to the drawing board and bring out a concise and clear answer to this heated debate. To grab the bull by its horns, insurance buyers feel betrayed by the insurance companies especially when they do not indulge in accidents that prompt the companies to reimburse compensations. The government must analyze this aspect and bring out a more customer oriented car insurance policy.

Auto insurance buyers who in most of their life time do not assume compensations of any nature during their driving history are dissatisfied by the way insurance companies use their premium contributions for their sole benefits. Aptly, there is a burning issue that needs to be resolved and this is; should insurance buyers receive a considerable amount of refund if they do not cause accidents or are not in any way compensated for personal body injuries or car damages within their driving experience?

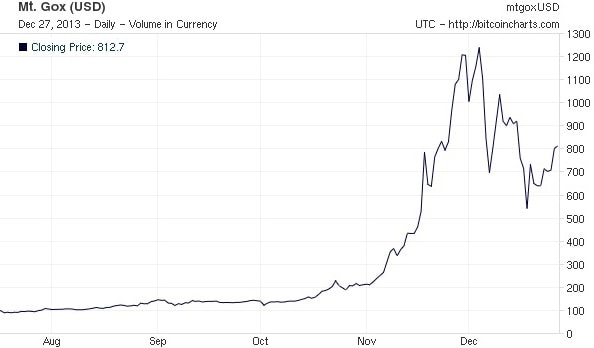

Little Known Bitcoins Gain Value by Over A Million Times ...Peaked At $1,250 in November 2013

A few years, if you were to buy a bit coin, you would get close to 1,000 bitcoins in every $1 US dollar. Today, a couple of years down the line, things have turned upside down and buying a single bitcoin will cost you more than $1000 dollars. The shift to using crypto currencies is creating a strong market for these kinds of virtual currencies.

And, as the head of currency research Bank of America Merrill Lynch said, bitcoins, the unregulated virtual currency might emerge as a serious competitor to the fiat or traditional money transfer providers.

Technology is behind the development of virtual currencies and one remarkable example is that of bitcoins. Bitcoins are today being used in trading foreign exchange and buying products online, and the popularity of this crypto currency is picking up so quickly yet strongly. More and more businesses and individuals are now becoming aware of the benefits of using the crypto currency over traditional currencies.

Although the value of bitcoins is constantly changing, it is heading on the higher scale, and as of November 2013, the virtual currency traded at close to $1300. This is an amazing growth considering that in just a few years, about $1000 bitcoins where trading for $1. There are more than $1.5 billion worth of the bitcoins in the market. Millions of transactions occur daily and there is no fixed price for the virtual currency. It depends on the rate at which the currency is trading in the market.

One difference between bitcoins and the traditional currencies is that this virtual currency is not printed by any centralized bank and no government or bank sets its value. The value of bitcoin fluctuates based on supply and demand. To get started using this type of virtual currency, you need to get a Bitcoin wallet. This is the first step in using the bitcoins.

There are different applications through which you can create your bitcoin wallet. A bitcoin wallet is like an app, which you can download and install in your computer or phone using a software wallet on the internet. Bitcoins can be obtained in different ways such as selling goods and accepting payment in form of bitcoins. More merchants are now doing this as they begin to realize the value and benefit of bitcoins.

You can also purchase and sell the bitcoins through virtual currency exchanges or Bitcoins exchanges. This is the common method used by people to obtain bitcoins. You have to be very careful when you trade online with bitcoins, as the frauds are ripe. You can also trade bitcoins with traditional currencies like US dollars.

Friday, January 03, 2014

How to Borrow a Suitable Car Loan and Safeguard Your Collateral

Collateral can be defined as the security assets that are placed against a loan by the borrower. Not all loans require collateral. Auto loan attracts collateral depending on the risk that is associated with the borrower in paying the loan. A client who has a bad credit score will attract higher interest rate on the loan granted.

Similarly, a bad credit score implies that there is a need for the borrower to provide security against the loan. Consequently a loan recipient who has a high credit score and less debts proves the ability to pay for loan thus may not be required to place collateral against the loan borrowed.

In order to safeguard your assets against possible repossession by a financial company, you should consider various factors which include borrowing depending on your pay back ability. A client with a sustainable stream of income and sizable monthly returns can go for short period high interest auto loans.

These are described as the unsecured auto loans. These are clients with high and stable incomes. The recession has virtually affected most clients despite their financial status and thus acquiring an unsecured loan means that you do not pose a risk on your assets.

Consequently depending on your income levels and the sustainability, you may opt to go for the secured loans due to the low interest rate associated with. However, you need to maintain a strict repayment program so that you do not result to delinquencies and possibly be unable to pay the loan leading to loose of your collateral.

If you have a low income but a sustainable, one you should consider the secured loan. In this case, your limited income can be able to pay the loan for a relatively long period on low interest rate. The recession has seen constraint in incomes and reduced business returns and most of the loans are attracting security. There is uncertainty in paying of the loans.

Moreover, those with well thriving incomes can still go for the unsecured auto loans. These attract high interest rates but the assets placed against the loan are not in a risk compared to the unsecured ones. Financial institutions are calling for open discussion in regard to auto loaning so that the borrower is aware of the implications resulting to the failure to meet the auto lenders loan terms and conditions

All the mentioned aspects are considered by borrowers in order to acquire a car loan that will place the clients in the best possible position to repay. Through these factors a client can measure the level of uncertainty associated with borrowing that may subject the collateral to risk of repossession by an auto finance company. The borrower can then acquire a car loan or forfeit it altogether.

Similarly, a bad credit score implies that there is a need for the borrower to provide security against the loan. Consequently a loan recipient who has a high credit score and less debts proves the ability to pay for loan thus may not be required to place collateral against the loan borrowed.

In order to safeguard your assets against possible repossession by a financial company, you should consider various factors which include borrowing depending on your pay back ability. A client with a sustainable stream of income and sizable monthly returns can go for short period high interest auto loans.

These are described as the unsecured auto loans. These are clients with high and stable incomes. The recession has virtually affected most clients despite their financial status and thus acquiring an unsecured loan means that you do not pose a risk on your assets.

Consequently depending on your income levels and the sustainability, you may opt to go for the secured loans due to the low interest rate associated with. However, you need to maintain a strict repayment program so that you do not result to delinquencies and possibly be unable to pay the loan leading to loose of your collateral.

If you have a low income but a sustainable, one you should consider the secured loan. In this case, your limited income can be able to pay the loan for a relatively long period on low interest rate. The recession has seen constraint in incomes and reduced business returns and most of the loans are attracting security. There is uncertainty in paying of the loans.

Moreover, those with well thriving incomes can still go for the unsecured auto loans. These attract high interest rates but the assets placed against the loan are not in a risk compared to the unsecured ones. Financial institutions are calling for open discussion in regard to auto loaning so that the borrower is aware of the implications resulting to the failure to meet the auto lenders loan terms and conditions

All the mentioned aspects are considered by borrowers in order to acquire a car loan that will place the clients in the best possible position to repay. Through these factors a client can measure the level of uncertainty associated with borrowing that may subject the collateral to risk of repossession by an auto finance company. The borrower can then acquire a car loan or forfeit it altogether.

How Businesses Can Reduce Computer and Internet Network Vulnerability

In defining what is computer network security, it is imperative to mention that it is the application of security techniques to reduce network vulnerabilities. These security techniques help in protecting the usability, integrity, reliability and safety of computer networks and data. A network security protects your computers from threats such as viruses, Trojan horses, worms, spyware and adware. It also prevents zero-day attacks, hacking attacks and denial of service-DoS attacks.

Moreover, these computer security systems also protect identity theft such as stealing of your names, addresses, phone numbers and your personal information. Network security systems include anti spyware, anti-virus, firewalls, intrusion prevention systems-IPS and virtual private networks-VPNs.

Loss of company information is one of the aspects, which place the survival of many businesses at stake and with breach of internet network security; businesses can lose data which cost them a penny. It is therefore essential for businesses to protect their data and information through computer network system protection.

Company data is not only threatened by physical intruders but also by internet and cyber war uncertainties. According to Forrester Research Incl., businesses in the world are losing close to about $221 billion in a year through data loss with the American businesses parting with about $54 billion due to loss of their company data.

At the same time, according to the ABI Research, businesses in the world are spending more than $6 billion a year in network and data-security technology and this figure is expected to rise to $ 10 billion by the year 2016. What this means is that businesses need to invest in data protection. The threat in cyber warfare is so real that every week there are news reports of companies and organizations from small businesses to the defense departments claiming to have lost their data.

The potential damage that is caused by such data loss goes far more than just lost or damaged data. For instance, information that is stolen amounts to lost intellectuality as well as jobs from the businesses since new product information can be stolen and shortly copies of that new product are found in other markets at very off the cuff prices.

One of the ways in which businesses can protect their computer network is through setting up a network breach prevention program. There is a need for businesses to define their computer and internet network security peripherals and put in place the best protection practices possible. There is a need to seek for internet services providers to establish, which IP addresses a business uses and also obtain proper permissions.

The IP addresses also need to be monitored so that the business can know when unused IP addresses suddenly come to use. All external network access points need to be managed through encrypted virtual private networks- VPNs and use of firewall. Two- factor authentication solutions help in providing secure remote access of networks. These authentications strictly control the access into your business network with authentication devices, passwords and account log in details.

The use of static passwords does not provide adequate security for your computer network. Gaining an unauthorized access to networks can be both simple and complex. In a simple way, ill-intended people can steal passwords to gain access to your network. On the other hand, they can use complex ways such as launching a Trojan or even a phishing attack.

The use of traditional static passwords is outdated and archaic and cannot effectively deter those using complex phishing and hacking techniques to penetrate internet network security systems and harvest confidential data. Statistics show that a shocking 43% of businesses who lose electronic data never reopen and that about 29% will close their businesses within two years, according to Researchers McGladrey and Pullen.

This shows the magnitude of the impacts of data loss in companies. Businesses can also protect their computer network through segmentation, which insulates the business from the risks. They can use firewalls to control the inbound and outbound traffic to their networks.

There should be internal network segmentation between different offices to help prevent breach of computer and internet network security. Businesses also need to use very strong encryption for their networks such as SSL. Last but not least, businesses should have a backup for their data through remote data backups. This can help in data recovery and retrieval when disasters strike and data is lost or damaged.

Moreover, these computer security systems also protect identity theft such as stealing of your names, addresses, phone numbers and your personal information. Network security systems include anti spyware, anti-virus, firewalls, intrusion prevention systems-IPS and virtual private networks-VPNs.

Loss of company information is one of the aspects, which place the survival of many businesses at stake and with breach of internet network security; businesses can lose data which cost them a penny. It is therefore essential for businesses to protect their data and information through computer network system protection.

Company data is not only threatened by physical intruders but also by internet and cyber war uncertainties. According to Forrester Research Incl., businesses in the world are losing close to about $221 billion in a year through data loss with the American businesses parting with about $54 billion due to loss of their company data.

At the same time, according to the ABI Research, businesses in the world are spending more than $6 billion a year in network and data-security technology and this figure is expected to rise to $ 10 billion by the year 2016. What this means is that businesses need to invest in data protection. The threat in cyber warfare is so real that every week there are news reports of companies and organizations from small businesses to the defense departments claiming to have lost their data.

The potential damage that is caused by such data loss goes far more than just lost or damaged data. For instance, information that is stolen amounts to lost intellectuality as well as jobs from the businesses since new product information can be stolen and shortly copies of that new product are found in other markets at very off the cuff prices.

One of the ways in which businesses can protect their computer network is through setting up a network breach prevention program. There is a need for businesses to define their computer and internet network security peripherals and put in place the best protection practices possible. There is a need to seek for internet services providers to establish, which IP addresses a business uses and also obtain proper permissions.

The IP addresses also need to be monitored so that the business can know when unused IP addresses suddenly come to use. All external network access points need to be managed through encrypted virtual private networks- VPNs and use of firewall. Two- factor authentication solutions help in providing secure remote access of networks. These authentications strictly control the access into your business network with authentication devices, passwords and account log in details.

The use of static passwords does not provide adequate security for your computer network. Gaining an unauthorized access to networks can be both simple and complex. In a simple way, ill-intended people can steal passwords to gain access to your network. On the other hand, they can use complex ways such as launching a Trojan or even a phishing attack.

The use of traditional static passwords is outdated and archaic and cannot effectively deter those using complex phishing and hacking techniques to penetrate internet network security systems and harvest confidential data. Statistics show that a shocking 43% of businesses who lose electronic data never reopen and that about 29% will close their businesses within two years, according to Researchers McGladrey and Pullen.

This shows the magnitude of the impacts of data loss in companies. Businesses can also protect their computer network through segmentation, which insulates the business from the risks. They can use firewalls to control the inbound and outbound traffic to their networks.

There should be internal network segmentation between different offices to help prevent breach of computer and internet network security. Businesses also need to use very strong encryption for their networks such as SSL. Last but not least, businesses should have a backup for their data through remote data backups. This can help in data recovery and retrieval when disasters strike and data is lost or damaged.

Great Tips on How to Get the Most out of a Trade Show

Despite the fact that trade show displays marketing strategy has a high cost of lead generation and qualification, when it is carried out appropriately, it has showed outstanding resilience in promotional activities. It has proved to be a great opportunity for meeting face-to-face with business partners and clients, something that lacks in internet promotional activities. In order to make your trade show a success, there are things that need to be observed by the trade show promotional team, which help in engaging, qualifying and disengaging the prospects.

The main goal for a trade show is to meet and qualify as many leads as possible, which can later be converted into sales. What this means is that the promotional team should focus on capturing as many leads as they can. The engagement time needs to be minimal and something close to 5 minutes may be regarded as an appropriate time that needs to be allocated for each engagement.

By waiting to convert leads after a trade fair helps in maximizing the number of booth visitors who are able to be qualified. It also helps to slowly nurture the lead prospects that have longer sales cycle time. The quality of leads that is generated from trade show displays continues to be one of the strongest and ranks among the most qualified.

When using trade show signage, you need not fill your booth with words. This is because, a trade fair booth is more of a billboard rather than a datasheet meaning that the booth should provide a selling environment. You should not wait for the visitors in your booth to stop by and start reading your signage as it is the role of the sales team to approach the visitors and to put across the message and product features.

A more aggressive face-to-face engagement is required to help qualify the leads. Moreover, the trade show signage should not be put below the table height as it may not be noticed or easily seen by visitors. The literature graphics as well as the booth appearance should match the look and message of your company website.

In addition, when on the trade show floor, the promotional team should not focus heavily on giving out the literature to unqualified leads since most of the literature that is collected from the shows never make its way to homes or offices. The trade show displays team can focus on obtaining emails and contacts of the prospects and promise that the literature will be send to them and therefore, they do not have to carry it.

One of the reasons why it is recommended not to close a sale with the qualified leads right on the trade show floor is that in general, trade shows convert only about 1-5% of the total number of visitors of a trade show booth. Attempting to close the sales during the show time can limit the team from qualifying a large number of visitors.

There is also need to use marketing automation strategies to help in nurturing the prospects to become sales. There are software programs, which can be used to generate tailored emails for those customers interested in your products and services but they are not able to make a buying decision right away at the trade show displays.

Using the software programs ensures that sales persons are readily involved when a lead is nurtured to a ready-to-buy status. This helps reduce the time which is wasted chasing after leads that are in the early stages of the sales cycle thus improving efficiency in lead qualification and conversion.

The main goal for a trade show is to meet and qualify as many leads as possible, which can later be converted into sales. What this means is that the promotional team should focus on capturing as many leads as they can. The engagement time needs to be minimal and something close to 5 minutes may be regarded as an appropriate time that needs to be allocated for each engagement.

By waiting to convert leads after a trade fair helps in maximizing the number of booth visitors who are able to be qualified. It also helps to slowly nurture the lead prospects that have longer sales cycle time. The quality of leads that is generated from trade show displays continues to be one of the strongest and ranks among the most qualified.

When using trade show signage, you need not fill your booth with words. This is because, a trade fair booth is more of a billboard rather than a datasheet meaning that the booth should provide a selling environment. You should not wait for the visitors in your booth to stop by and start reading your signage as it is the role of the sales team to approach the visitors and to put across the message and product features.

A more aggressive face-to-face engagement is required to help qualify the leads. Moreover, the trade show signage should not be put below the table height as it may not be noticed or easily seen by visitors. The literature graphics as well as the booth appearance should match the look and message of your company website.

In addition, when on the trade show floor, the promotional team should not focus heavily on giving out the literature to unqualified leads since most of the literature that is collected from the shows never make its way to homes or offices. The trade show displays team can focus on obtaining emails and contacts of the prospects and promise that the literature will be send to them and therefore, they do not have to carry it.

One of the reasons why it is recommended not to close a sale with the qualified leads right on the trade show floor is that in general, trade shows convert only about 1-5% of the total number of visitors of a trade show booth. Attempting to close the sales during the show time can limit the team from qualifying a large number of visitors.

There is also need to use marketing automation strategies to help in nurturing the prospects to become sales. There are software programs, which can be used to generate tailored emails for those customers interested in your products and services but they are not able to make a buying decision right away at the trade show displays.

Using the software programs ensures that sales persons are readily involved when a lead is nurtured to a ready-to-buy status. This helps reduce the time which is wasted chasing after leads that are in the early stages of the sales cycle thus improving efficiency in lead qualification and conversion.

Subscribe to:

Posts (Atom)